Thai Baht Opens at 33.42 Baht per Dollar, Slightly Weaker and Nearly Unchanged

Mr. Poon Panichpipat, a strategist at Krungthai GLOBAL MARKETS, revealed that the Thai baht opened this morning at 33.42 baht per dollar, "slightly weaker and nearly unchanged" from last week's closing level of 33.37 baht per dollar. Since Friday night, the baht (USDTHB) has moved without a clear direction within a sideways range (fluctuating between 33.32-33.43 baht per dollar), receiving some support from the gradual rebound in gold prices (XAUUSD), which managed to swing above the $4,000 per ounce zone again. However, the baht faced some depreciation pressure in the Asian financial market this morning amid uncertainties surrounding the situation in the Middle East, following the outbreak of hostilities between the U.S. and Iran since last Friday (with details of the U.S. attacks released after the financial markets closed), supporting a gradual strengthening of the dollar and putting pressure on gold prices to decline.

Last week, the improving navigation through the Strait of Hormuz pressured crude oil prices, leading market players to gradually reduce the likelihood of the Fed raising interest rates.

For this week, including the short term, we assess that it is important to monitor developments in the Middle East, which remain highly uncertain, while also awaiting U.S. labor market data and statements from key central bank officials at the ECB seminar in Sintra.

Global Economic Outlook

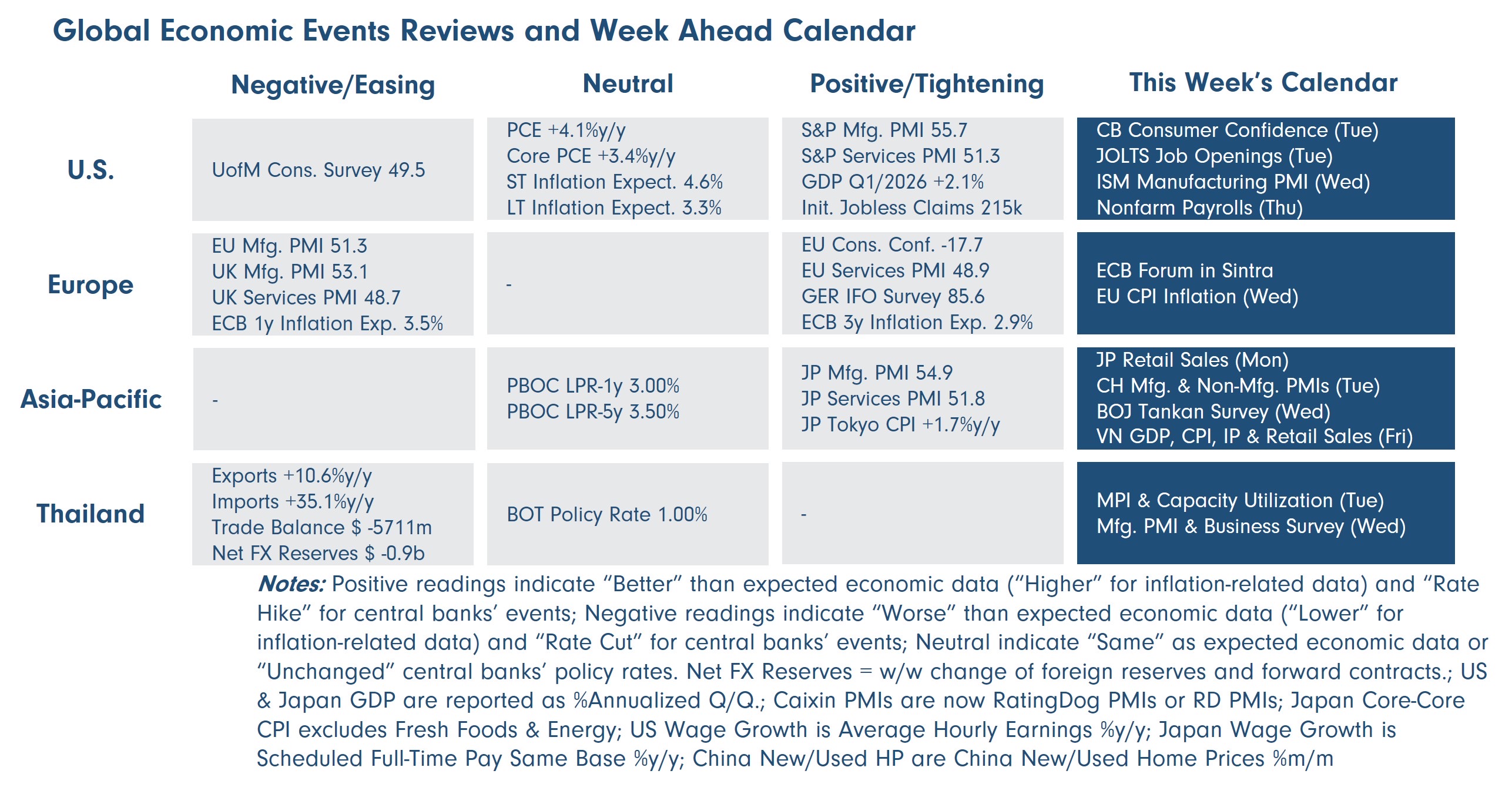

- U.S. – The situation in the Middle East is expected to become a key issue that market players will closely monitor, potentially creating significant volatility in the financial markets. Recently, tensions in the Middle East have escalated, particularly regarding navigation through the Strait of Hormuz. In terms of economic data, the highlights will be the U.S. labor market report, including non-farm payrolls, unemployment rate, and wage growth. During this period, we believe market players may focus on wage growth rates and the tightness of the U.S. labor market, which should be assessed from job openings (JOLTS) and the quit rate, as this data may reflect risks of rising inflation in the U.S. or the potential for a second-round effect and wage-price spiral, which could necessitate the Fed to raise interest rates as the market expects. According to the latest dot plot, market players estimate a 26% chance that the Fed will raise rates twice this year (the likelihood of rate hikes has been gradually decreasing due to falling crude oil prices and the latest PCE inflation report coming in as expected).

- Europe – The key highlight will be the central bank seminar hosted by the European Central Bank (ECB) in Sintra, Portugal, where market players will await statements from central bank officials from both the ECB and the Bank of England (BOE) to assess the outlook for monetary policy. Additionally, market players will be looking forward to the Eurozone inflation report for June, which may determine the ECB's monetary policy direction, as market players still believe there is about a 96% chance that the ECB will proceed with another rate hike of +25bps in the December meeting.

- Asia – Market players will be assessing the economic outlook for Japan and the direction of the Bank of Japan's (BOJ) monetary policy through reports on retail sales and industrial production for May, along with the BOJ's business sentiment survey (Tankan Survey). In China, market players will evaluate the recovery of the Chinese economy through the manufacturing and services PMIs for June, particularly focusing on the RatingDog PMIs that emphasize small and medium-sized enterprises. In Vietnam, market players will be looking forward to the Q2 GDP growth report and key economic data for June, such as export figures, retail sales, and CPI inflation rates.

- Thailand – Market players will be monitoring reports on Thailand's industrial production, such as the manufacturing PMI for June, the manufacturing production index (MPI), and the capacity utilization rate for May. Although Thailand's export figures have been continuously growing amid the AI boom, the overall manufacturing sector has not shown clear signs of continuous expansion, reflecting that some of Thailand's export goods are imports from abroad for re-export without significant domestic production or value addition. Additionally, Thailand's manufacturing sector continues to face pressure from cheap imported goods.

Regarding the outlook for the baht, we believe that although the momentum of the baht's depreciation (USDTHB) has slowed down somewhat towards the end of last week, it still has strength, making it likely for the baht to gradually weaken or at least fluctuate within a sideways range. The baht may weaken past the resistance zone of 33.50 baht per dollar and could continue to weaken to test the resistance zone of 33.75 baht per dollar easily if the U.S. economic data comes out better than expected, coupled with an intensifying situation in the Middle East that supports rising energy prices, leading market players to worry about inflation trends and adjust the likelihood of Fed rate hikes from the current 28% chance of two rate increases. In this scenario, we should see gold prices (XAUUSD) decline sharply, breaking below the $4,000 per ounce support level again. However, if market players reduce the likelihood of Fed rate hikes and the financial market atmosphere begins to accept more risk (be cautious of a stronger dollar if the market turns risk-averse, such as a global tech stock sell-off), the baht may strengthen somewhat, but could face resistance around 33.00 baht per dollar (next support at 32.75-32.85 baht per dollar).

We emphasize that the baht still faces two-way risks and can move in both directions depending on the situation in the Middle East and the monetary policy direction of major central banks, especially the Fed, where market players will be awaiting every important U.S. economic report, particularly inflation data. If market players gradually adjust their expectations for Fed rate hikes, we believe the baht could easily strengthen again. Conversely, the baht may also risk further depreciation (initially estimated that a 60% adjustment in the likelihood of Fed rate hikes could pressure the baht to weaken or strengthen by about 30 satang). Given the current high volatility of the baht, we reiterate our previous recommendation that market players should employ diverse risk management strategies, such as using options strategies to enhance risk management efficiency amid high market volatility.

Technically, if assessed using a trend-following strategy, the baht (USDTHB) remains in a weakening trend and will continue in this trend until it can strengthen past the 32.50 baht per dollar zone clearly and consistently (watch the 30-week moving average support around 32.30 baht per dollar), which may lead the baht to gradually weaken or at least fluctuate sideways within a broader range.

As for the dollar, we believe it may strengthen somewhat if market players increase the likelihood of the Fed raising rates in the event that the situation in the Middle East escalates again, along with U.S. economic data continuing to come in better than expected and reflecting a strong economy. However, the two-way risk remains.

We see the baht's range this week at 33.00 - 33.75 baht/dollar.

For the baht's range in the next 24 hours, it is expected to be at 33.30 - 33.50 baht/dollar.